LE’s New Business Opportunities

Your quarterly pulse on hotel development trends and LE news

China Room Counts Reach All-Time High in Q3’21

In the recently released China Construction Pipeline Trend Report by Lodging Econometrics (LE), at the end of the third quarter of 2021, China’s total construction pipeline stands at 3,571 projects/681,095 rooms, up 5% by projects and 7% by rooms year-over-year (YOY). Rooms in the country’s hotel construction pipeline are at an all-time high, and the pipeline is a mere three projects shy of the cyclical high of 3,574 projects set in the second quarter of 2020.

While the COVID-19 pandemic continues to plague the global hospitality industry, China is showing signs of recovery. Large-scale vaccination rates, as well as increases in local tourism, have led to growing booking and occupancy numbers over recent months. Further, developers and investors have remained active and hotel development continues to thrive throughout the country. At the end of the third quarter, new project announcements increased a substantial 52% over Q2‘21. Additionally, brand conversion and renovation activity remains strong in the region.

There are presently 2,453 projects/444,439 rooms under construction in China, up 11% by projects and 10% by rooms YOY. Rooms under construction reached record totals in Q3. Projects scheduled to start construction in the next 12 months are at 546 projects/103,526 rooms, down 27% by projects and 15% by rooms YOY. Project and room counts in the early planning stage each recorded record highs, up 26% by projects and 25% by rooms YOY, standing at 572 projects/133,130 rooms at the end of Q3. The upscale and upper midscale chain scales both hit project and room count peaks this quarter and account for over half of China’s construction pipeline.

Through the third quarter of 2021, China has opened 416 hotels/67,913 rooms. The LE forecast for new hotel openings expects another 345 hotels/45,050 rooms to open in the fourth quarter, bringing the expected new hotel openings to 761 new hotels with 112,963 rooms by year-end. In 2022, 920 new hotels with 150,899 rooms are forecast to open.

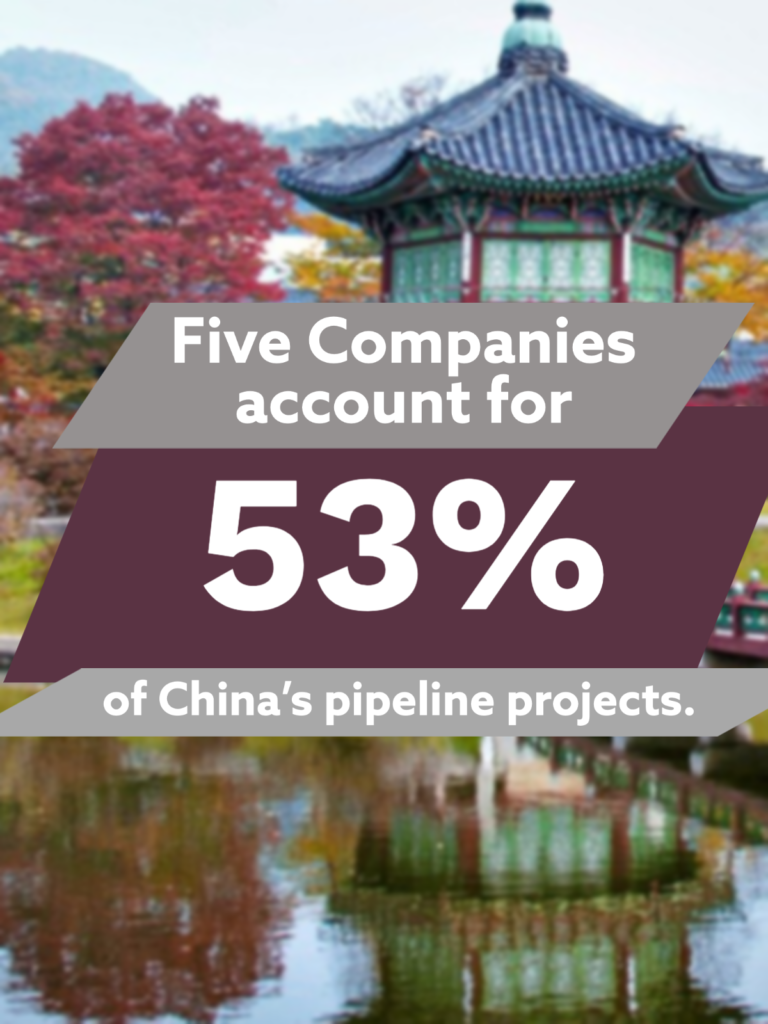

Five companies account for 53% of the projects in China’s total Q3 construction pipeline

The top hotel franchise companies in China’s Construction Pipeline are Hilton Worldwide with record highs of 666 projects/124,602 rooms, InterContinental Hotels Group (IHG) with 443 projects/91,077 rooms, Marriott International with 391 projects/104,674 rooms, JinJiang Holdings with 204 projects/20,195 rooms, and Accor with 178 projects/31,996 rooms. These five companies account for 53% of the projects in China’s total Q3‘21 construction pipeline.

The largest brand in the Pipeline for each of these companies are Hampton by Hilton, with 375 projects/56,798 rooms. Hilton Garden Inn with 85 projects/17,447 rooms. Each of these brands hit cyclical peaks in the third quarter and account for 69% of Hilton’s total construction pipeline in China. IHG’s most prominent brands at the end of the Q3 are Holiday in Express with 203 projects/33,636 rooms and Holiday Inn with 71 projects/17,284 rooms. The top brands for Marriott International are Four Points Hotel with record counts at 64 projects/17,443 rooms and its Marriott Hotel brand with 59 projects/17,948 rooms. Leading brands for JinJiang Holdings are 7 Days Inn with 101 projects/7,951 rooms, followed by Vienna Hotel with 44 projects/4,502 rooms. Accor’s leading brands are the Ibis brands with 60 projects/6,338 rooms and Mercure Hotel with 49 projects/7,922 rooms.

Chengdu has all-time highs by both projects and rooms in Q3

China’s total construction pipeline is led by Chengdu with all-time highs by both projects and rooms of 140 projects/28,643 rooms. Following Chengdu is Shanghai with 127 projects/24,768 rooms, then Guangzhou with 121 projects/24,791 rooms, Wuhan with 98 projects/13,533 rooms, and Xi’an with 94 projects/16,785 rooms.